2020 Performance and lessons learned

By all accounts, 2020 was a ridiculous year in markets. We saw a global pandemic trigger the fastest market meltdown since the great depression, followed by a gravity defying moon shot that took us to all-time highs just months later.

That said, given the outlier nature of 2020, I think it’s particularly important to take stock of what we investors did well in 2020 and what we didn’t do so well. When looking at a year like 2020 -with a bounce off the bottom- it’s easy to attribute good returns to skill when it’s just as likely luck. It’s smart to be critical of our decisions, to improve future judgements. Here is a summary of my 2020 moves:

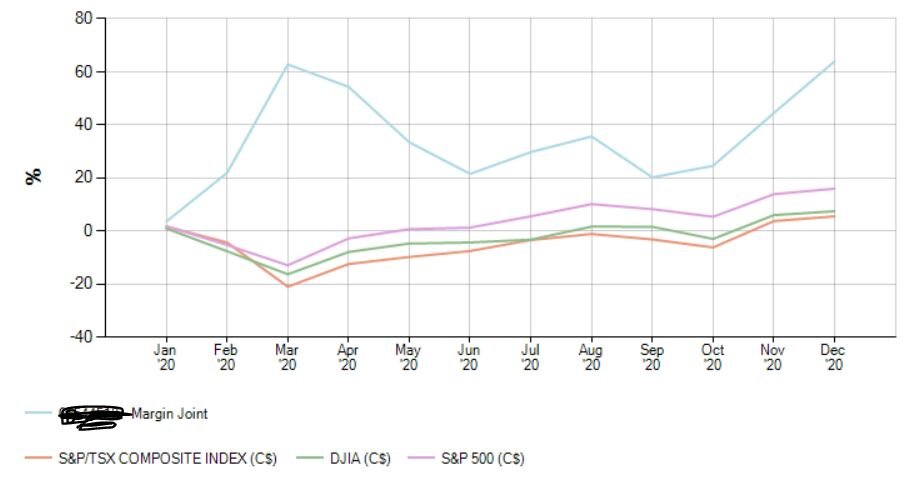

Total return 2020 – 63.99%

This year I had a few big winners and a couple of big stinkers I am not likely to forget.

Win – Granite Oil Corp. - up 56.5%

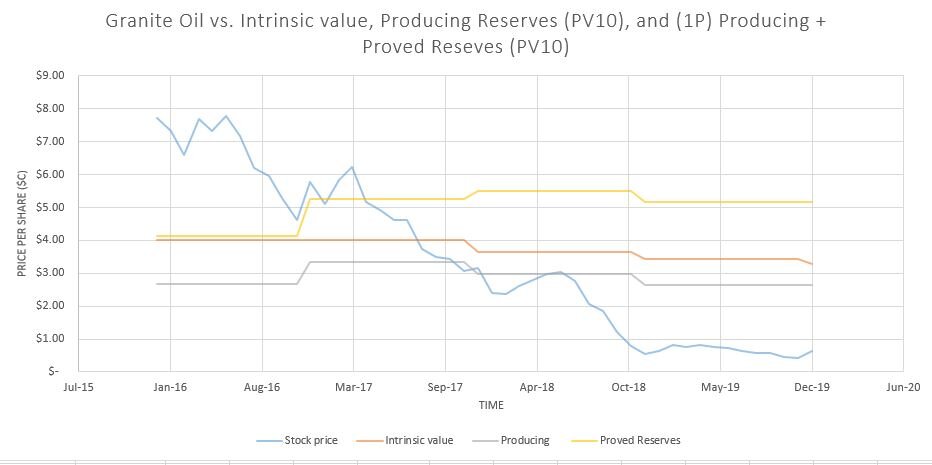

In December of 2019, a tiny ($23M market-cap/$65M EV) Canadian oil producer by the name of Granite Oil came onto my screens. The company owned some low decline oil assets in southern Alberta and happened to be undergoing a waterflood program.

What made it interesting was it’s low decline assets that gushed cash-flow, even at relatively low oil prices. Management had seen the pain over the past year and were intent on paying down debt and would be able to do so within a few years. The equity traded at a 44% free cash flow yield at the time. Yes you read that right. Nobody wanted it. When doing the math at the time the NPV10 of producing reserves after debt came to a share price of $2.64. My cost basis was $0.60/share and I was buying it in size. The market for the shares was so thin I had to wait days not hours to sometimes close my limit orders. Then on January 20th, the company announced it was being bought by International Petroleum Corp. (IPCO) for $0.95/share in cash. My intrinsic value calculation below:

What I did well:

-I identified an average, low-decline asset that was un-ownable by the big guys, due to its size and waited for things to improve.

What I did wrong:

-Bought too much. Just a month later, the market was in chaos due to Covid and it’s likely that Granite would have gotten crushed like every other E&P. Certainly got lucky given the timing on this one.

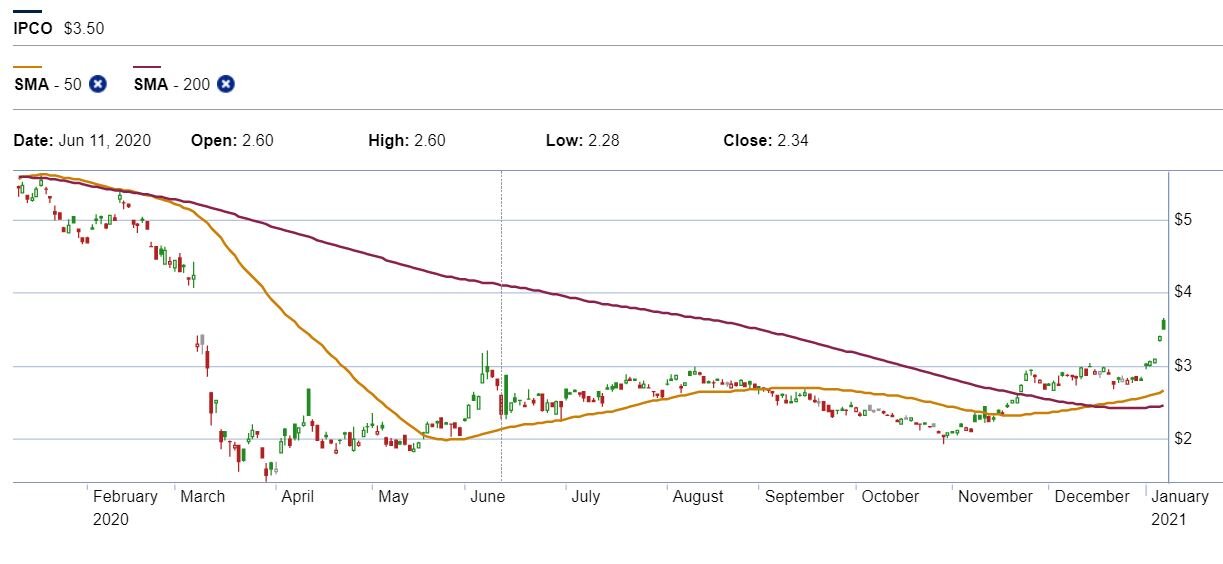

Loss – International Petroleum Corporation (IPCO)– down 33.36%

To be honest, the sale of Granite sort of irked me. While proud of the win, I was still a little pissed that it sold for so little. My intrinsic value of the company was 6X my purchase price and it only sold for a 56% premium?!? Damn people hate oil. But after the deal I looked deeper into the buyer IPCO and found that it owned some decent Canadian oil assets and some okay European assets, had conservative management, and a B+ balance sheet. For what I believed at the time was a market bottom, this looked to be a winner.

Furthermore, they were getting Granite for a song and based on my math, IPCO was also trading at a significant discount to fair value. I bought a material position (though less than half the size of my Granite investment).

Then shit hit the fan and confronted by the unprecedented collapse in oil/gas prices in early March, I was concerned that the assets IPCO owed were okay, but perhaps not good enough in a world where nobody drives to work or flies for business anymore. So there I was in early March already doing tax loss selling. Seriously, what a fucking disaster.

But that wasn’t the only reason I sold. There was at the time what I believed to be a massive opportunity to upgrade the portfolio. I used some of the proceeds in the following weeks to buy into my favorite Canadian oil/gas companies including the GOAT, the Canadian Vampire Squid itself: Canadian Natural Resources in the low teens, a price I do not suspect we’ll ever see again. *Knock on wood*

What I did right:

- I followed my inner Paul Tudor Jones and reduced the size of the position , as price fell.

- Took advantage of a bad situation to move into a higher quality asset that had fallen nearly as much.

- Realized a capital loss to off-set taxable gains incurred on Granite sale.

What I did wrong:

- The downside support in IPCO broke on March 10th. It took me 3 more days to talk myself into selling the last of my position. I estimate that mistake cost me 8% of the total (33%) loss. Damn that was stupid

Win – Tesla, Live Nation, XOP (US E&P ETF) – PUT and PUT spreads - up 50.5%

Just like you want some defenders and a goalie on your hockey team, I’m never full on 100% long in my portfolio. However, given the cost of maintaining short positions, I generally try to hold deep OTM puts and then tactically short at times where it looks like the market could conjure it’s inner Icarus. Luckily, I had some insurance in preparation for the February down-turn.

My hedge book included a few shorts but mostly some out of the money options on assets I thought would get beaten up by a pandemic triggered market collapse. Something about people being welded into their homes in China made me think twice. I got lucky (while the whole world got crushed) and the proceeds on the contracts allowed me to be an investor in April/May, when others were just trying to recoup losses.

What I did right:

- I maintained a tactical down-side hedge book and added to downside assets, as events got progressively worse.

- I closed on many of my positions in mid-March (sold many of my Tesla contracts on March 16th) when volatility nearly top ticked, one contract at a 614% return. Crazy

What I did wrong:

- I initiated some PUT spreads in April and May in anticipation of a re-test. I was too busy listening to the Real Vision guys talk about the world ending and not enough time reading charts. I held onto these subsequent positions to long and it limited the gains on these trades.

Win – Canadian oil and gas – CNQ/Parex/Whitecap/Tamarack Valley – up 37%

I’ve grouped these securities together, as they were discussed in past blog posts:

https://thedutchexplorer.ca/blog-2/consolidation-agency-and-a-prisoners-dilemma

https://thedutchexplorer.ca/blog-2/bullies-betas-and-ugly-trees

https://thedutchexplorer.ca/blog-2/alpha-fragility-and-the-vampire-squid

I loaded up on Canadian energy in 2020 and while it has taken some time to get going, it has been nothing but up since the vaccine announcements in November. They are still unbelievably cheap, relative to their historical values. I expect all the ones I own will be able to return capital to shareholders in 2021 (if not already). The real question is whether there is further consolidation, which would continue to help the industry and my bull thesis. Either way, I have not been this bullish on a particular market segment in a long time. These securities are my biggest positions.

What I did right:

-Bought some in March when the world thought oil was never going to be used again.

What I did wrong:

-Bought more in March.

Loss – Brighthouse Financial Inc. – down 31%

Another one of my Idiosyncratic plays that I worked on pre-covid. This is a business that trades at an obscene discount to book, let alone market that very few people understand. The problem was, the books are an absolute mess and it’s in a slow growth industry. The books are so ugly that most analysts that cover it don’t understand the accounting.

Regardless, the entire insurance industry was in trouble in early March when the Fed stated that interest rates would be pinned at zero for the foreseeable future. The problem being that these companies effectively earn money from (1) fees and (2) the interest earned on their float. The value of the fixed income portion of their float was in serious peril and I closed the position at a three-handle loss. Just a nightmare.

What I did right:

- I sold a business that was at risk of permanent loss of capital (see Buffett selling airlines) so I could fight another day.

What I did wrong:

- The thesis to own it required a turn in declining interest rates that has been persistent since 1981. Low probability.

- Owning shares in a business that only an accountant can understand is not in alignment with the current zeitgeist.

- Similar to the IPCO loss, I didn’t cut it soon enough, It broke the 200 day a full 4 days before I closed my last position costing me at least another 5%.

Win – Uranium – HURA ETF – up 41%

HURA ETF is my core position in how I’m playing the Uranium bull market. I first initiated a small position in the ETF back in 2018. At that time, the market was slowly grinding lower, but I wanted to be a tune with the space. The best way to give yourself an incentive to do more work is to buy a small block of what interests you. Since the March lows I have been adding steadily. Also own some PDN and NXE.TO.

Similar to Canadian energy, there isn’t much more I need to say about Uranium. See last week’s post for more details: https://thedutchexplorer.ca/blog-2/fear-density-and-yellow-cake

What I did right:

- I waited for the market to give me the breakout signal and fundamental signal (mine closures) that the bear-market was nearly over before getting into a decent position.

What I did wrong:

- Traded around my Paladin position which I should have just sat tight as missed a couple of big days in November instead of just sitting tight.

Win - Antero Resources up 96%

When it became apparent that the shale oil companies were going to shut in wells, I initiated positions in several U.S. Midwest natural gas players.

Post the June surge in natural gas companies I dumped the whole basket except Antero Resources which I’ve held through December. Given that it's 100% hedged in natural gas combined with the dramatic rise in the price of propane use, the company has done exceedingly well in this difficult environment. It’s currently generating significant free cash flow at strip and despite a lot of debt (they are terming it out) I remain bullish long-term. In particular, I look forward to winter 2021/2022, when gas inventories have a real chance of becoming very tight.

What I did right:

- Bought a collection of names to take advantage of the bounce and remove some of the idiosyncratic risk in the trade.

What I did wrong:

- I did not fully comprehend the scale of the propane story (outside heaters are in high demand) until it had already ran-away on me so I didn’t get in as big of a position as I would have hoped to.

While the term-of-the-year might have been “social distancing”, I still think unprecedented is the most apt (if not most overused) word to describe this chaotic year in the markets. That said, when looking back on what I did wrong, many of them seem to relate to better trading vs. investing required in 2021. But it could also just have been the unprecedented times. Reminder, the above is not investing advice.

Best of luck in 2021!

The Dutch Explorer.